Coined by Sir

Mervyn King, the maradonian theory of interest rates holds that a central bank may

let expectations of economic agents work to its advantage instead of acting. An

avid fan of soccer himself, Sir Mervyn actually derived his theory from one of

the most astonishing goal runs made by Diago Maradona where he single handedly

beat five English midfielders to score one of the most celebrated goals in the

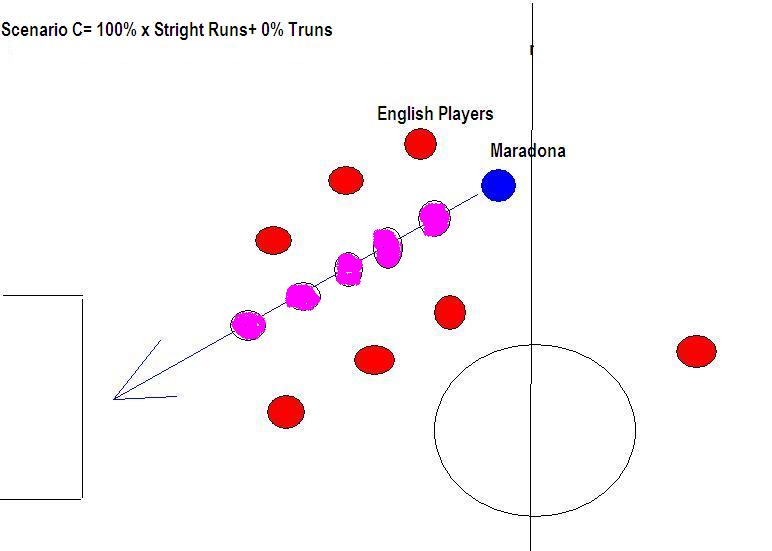

history of soccer. He argued that after receiving the ball near centerline,

Maradona -famous for his turns and dribbling moves- interestingly made a

straight run towards the English goal. The English midfielders, who were

expecting him to make usual fast turns, were taken by a complete surprise.

Likewise he argued

that a central bank, after fueling expectations about interest rates, doesn’t

necessarily needs to act since economic agents start making behavioral

adjustments under expectations. To what extent he can be agreed with, is

debatable. I will try to put forth both arguments for and against this in the

later section.

A fact that has

certainly worked to the advantage of Central banks has been that inflation hasn’t

picked up. While Ben, Dragi and King may attribute this to central bank’s

credibility, softening commodity and oil prices, household deleveraging and

sluggish global growth did play their role in keeping the aggregate demand

subdued especially in developed economies. Secondly and importantly, the

inflation expectations didn’t pick up despite Central Banks launched rounds

after rounds of their analogs Quantitative Easing program –interestingly, BoJ

is now being pressed for an open ended QE by political policymakers-. Despite

all odds, Central Banks did succeed in keeping the monetary policies accommodative

yet at no risk of inflation –the only exception is BoE where inflation remained

over inflation target for an intended period subsequently softening-

However, one

should ask himself if Maradona scored such a spectacular goal again? Or putting

in literal words can a central bank can just ‘cheat’ an extended period of time

by not acting? Answer is quite obvious. A simple example used in Macroeconomics

is the impact of central bank’s credibility over labor supply. It says that

economic agents engaged in labor initially increase their labor supply given

central bank outsmarts them by allowing a higher inflation. Result is an

increased labor supply and increased output at higher prices, leading to an

expansion. However, as the central bank keeps outsmarting them, the ultimate result is the demands for wage

indexation or a decreased supply or labor hours since the labor’s price for

labor falls relative to leisure, resulting in people preferring not to work.

To further

elaborate why Maradona can’t always make a blistering run consider the market as

English players and maradona as central bank. In scenario A markets are so used

to central bank’s credibility that they virtually neglect the possibility that

central bank would cheat them.

This given central bank a chance to ‘cheat’ them,

resulting in higher economic activity at higher inflation which agents consider

exogenous rather than a direct result of central bank’s actions. However, given

central bank repeats the strategy and defeats the expectations of economic

agents, economic agents start to price in the possibility of “cheating” and

start positioning them for inflation (Scenario II).

The more central bank doesn’t

act, the weaker the credibility grows and less effective central bank becomes

for an economy since if the cheating behavior becomes obvious, the agents start

seeking inflation protection (Scenario III).

This is quite obvious from the

subsequent rounds of QE by central banks which has fueled more inflation

expectations than initial ones because markets came to realization that “Bazooka”

with the central bank no longer works.

So can maradona

help policymakers? Yes it surely can. However, can it always help policymakers?

The answer depends upon till how long it can pull out the same stunts while

keeping others dumb. In Next post I will try to post some of the empirical

evidences for this phenomenon.

(This work in an intellectual property of Author,

I have no issues with the material being used given accompanied by a proper

acknowledgment of source)

No comments:

Post a Comment